IR35 has been around since 2000. Most UK businesses still get it wrong. Not because the IR35 rules are impossible to follow, but because most guidance treats IR35 payments as a paperwork problem. They aren’t.

The contract you sign with a contractor is the start of the story, not the end. What HMRC cares about is the working relationship that develops afterwards. That gap, between what the contract says and what people actually do, is where most companies fall over.

This guide takes a different angle. It explains the off-payroll working rules in plain English, looks at what real cases tell us, and then focuses on the part most articles skip: how to keep your contractor arrangements compliant after the ink dries.

Chapter 1: What the IR35 Rules Mean for Limited Company Contractors and Off-Payroll Working

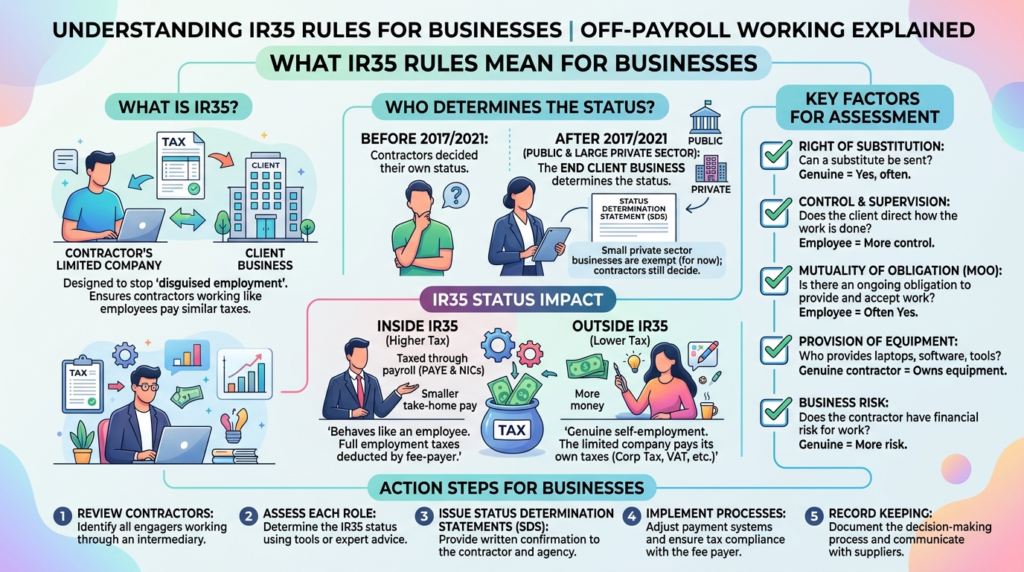

IR35 is shorthand for a set of UK tax rules. It targets people who work like employees but provide services through a limited company, often called a personal service company (PSC) or service company. The rules ask one question: if you stripped away the company, would the worker look like your employee?

If the answer is yes, the engagement is “inside IR35”. IR35 payments are then taxed roughly the same way as employment income, with income tax and national insurance contributions deducted at source. If the answer is no, the engagement is “outside IR35”, and the contractor working through a limited company keeps its more tax-friendly setup.

Who Is Responsible for Determining Employment Status?

Until 2017, contractors were responsible for determining their own IR35 status. Then HMRC moved that responsibility onto the end client in the public sector. From 6 April 2021, the same shift hit medium and large private sector businesses.

If you are a medium or large client, you must:

- Determine the IR35 status of each engagement — deciding whether it is inside or outside IR35

- Issue a Status Determination Statement (SDS) to the contractor and any agency in the chain

- Operate PAYE on IR35 payments if the role is inside IR35, ensuring you deduct income tax and national insurance contributions

- Run a process to handle disputes

Small companies are still exempt. The IR35 rules apply using the same definition of “small” as the Companies Act 2006, with the financial thresholds raised from 6 April 2025. Because IR35 looks back at your previous financial year, the practical effect of the new threshold won’t kick in for most affected businesses until the 2027/28 tax year.

The April 2024 Offset Rule Changed Everything for IR35 Payments

For years, businesses lived in fear of IR35 because of a quiet flaw in the IR35 legislation. If HMRC found you had wrongly placed a contractor outside IR35, you owed the full PAYE bill on IR35 payments, even though the contractor had already paid tax through their PSC. Two parties, one set of work, two tax bills.

Industry experts called it a 4x multiplier. Real liability of, say, £100,000 of underpaid tax could turn into a £400,000 settlement.

That changed on 6 April 2024. The Finance Act 2024 introduced an offset rule. HMRC now credits the tax already paid by the contractor’s PSC against the client’s IR35 payments bill. The financial risk dropped, in rough terms, by about 75%. Independent analysis suggests the real exposure is now closer to 10% of fees, not the 50% it once was.

This matters for your risk calculation. The reason many firms banned contractors entirely after the IR35 changes in 2021 was the size of the potential bill, not the chance of getting caught. With the offset in place, the maths now favours engagement over tax avoidance through blanket bans.

Table 1: How the IR35 Payments Risk Position Has Changed

| Item | Before April 2024 | From April 2024 |

|---|---|---|

| Liability if wrong | Full PAYE on gross fees | PAYE less tax already paid by PSC |

| Practical multiplier of underpaid tax | Around 4x | Around 1.1x |

| Effect on hiring | Many firms banned PSCs | Renewed willingness to engage |

| Penalties and interest | Still apply | Still apply |

| Effect on small companies | Out of scope (Chapter 8 applied) | Same, threshold raised April 2025 |

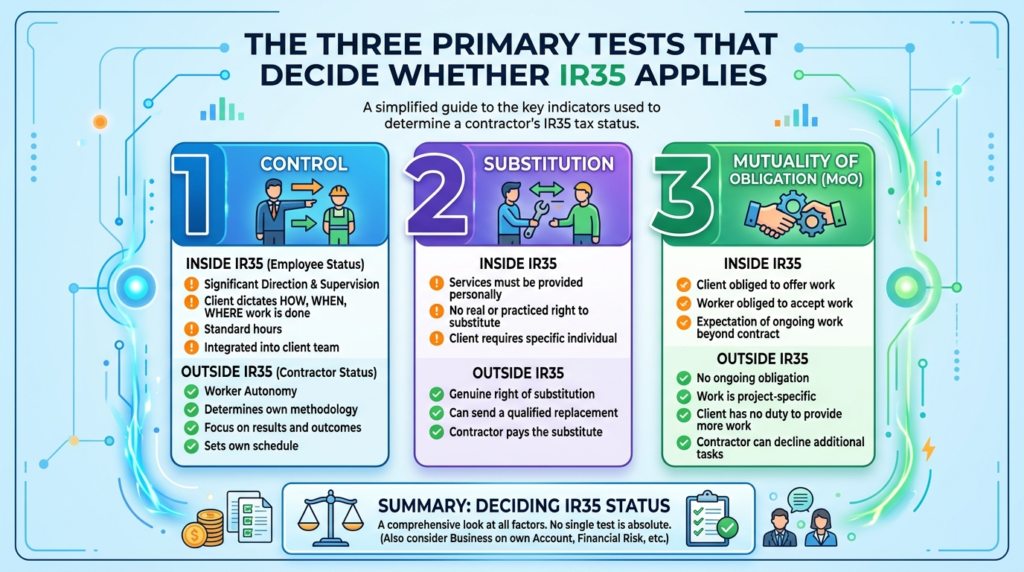

Chapter 2: The Three Tests That Decide Whether IR35 Applies

HMRC and the courts use a body of case law going back to the 1968 Ready Mixed Concrete decision to determine employment status for tax purposes. Three tests do most of the heavy lifting.

Mutuality of Obligation and the Off-Payroll Working Rules

This asks whether each side is bound to the other. Are you obliged to provide work? Is the contractor obliged to do it personally? The Supreme Court ruling in HMRC v Professional Game Match Officials Ltd in September 2024 gave clear guidance: a basic exchange of work for pay is enough to establish mutuality within an individual engagement. That doesn’t make someone an employee on its own, but it crosses the first hurdle.

Many contractor contracts try to avoid mutuality with phrases like “the company is not obliged to offer work and the contractor is not obliged to accept it”. After PGMOL, those clauses help less than people thought. Once the contractor accepts a piece of work and you pay for it, MOO exists for that engagement — and IR35 payments obligations may follow.

Control: How IR35 Rules Apply in Practice

This looks at how, where, when and what the contractor does. The more you control these elements, the more they look like an employee — and the more likely the contract is inside IR35. A genuine contractor sets their own hours, picks their methods, and works on their own terms within agreed deliverables.

The Atholl House case (Kaye Adams) made an important point. Control needs to be looked at across the whole picture, not just whether the client could in theory tell the contractor what to do. Many contracts give the client wide rights of control that are never exercised. Courts will sometimes look past unused powers, but only if the working reality clearly shows independence.

Personal Service, Substitution and the Service Company

A real contractor can send someone else to do the work through their service company. An employee cannot. A genuine right of substitution, one that the contractor could actually use, points hard towards self-employment and helps demonstrate a contract falls outside IR35.

But “genuine” is the key word. If your contract says substitution is allowed only with your written approval, and that approval is never given, the right is a fiction. Courts can and do look behind paper rights to working reality when determining the employment status of the worker.

The Fourth Factor: In Business on Own Account

Beyond the three core tests, courts consider whether the worker runs their own genuine business. Multiple clients, marketing, business risk, owning equipment, and taking financial risk all point to self-employment. This is what saved Kaye Adams. The First-tier Tribunal accepted that she had a 20-year freelance career, providing services to a client like the BBC that made up less than half her income.

Table 2: What Contracts Say Versus What Courts Examine

| Test | What contracts often say | What courts actually look at |

|---|---|---|

| Mutuality | “No obligation to offer or accept work” | Whether work-for-pay exchange exists in each engagement |

| Control | “Contractor has discretion over methods” | How the work is supervised in practice; reporting lines |

| Substitution | “Contractor may provide a substitute” | Whether substitution has happened or could realistically happen |

| In business on own account | “Contractor operates as an independent business” | Other clients, equipment, marketing, financial risk, business identity |

Chapter 3: What Real Cases Tell Us About IR35 Payments

The IR35 case law of the last few years is a goldmine for businesses that want to avoid the same mistakes. Here are the most useful ones.

HS2 Ltd: £6.2 Million in IR35 Payments for Trusting CEST

High Speed 2, the rail infrastructure project, paid HMRC £6.2 million in 2024 to settle a long-running compliance review of IR35 payments. The original 2022/23 provision was £10.2 million. HS2 had relied on HMRC’s own Check Employment Status for Tax (CEST) tool to assess its contractors and got the answers wrong.

The lesson is brutal. CEST is a guidance tool, not a defence. If your only compliance evidence is a CEST printout, you are exposed. By the year ending March 2024, HS2 was placing 94% of its contractors inside IR35 — meaning payments made through payroll with income tax and national insurance deducted. That swing tells its own story.

DWP, Ministry of Justice, Home Office: Public Sector IR35 Payments Failures

Three central government departments racked up combined IR35 payments settlements running into hundreds of millions:

- Department for Work and Pensions: around £87.9 million

- Ministry of Justice: about £72.1 million plus a £15 million fine

- Home Office: roughly £29.5 million plus a £4 million fine

Each had used CEST. Each had been described in HMRC reports as “careless” in their status determination assessments. Public sector bodies tend to be the test bed for IR35 enforcement before the same approach reaches private sector firms.

Atholl House (Kaye Adams): When a Contract Falls Outside IR35

This case ran for nearly a decade across four tribunal levels. HMRC pursued Kaye Adams over BBC radio work. She finally won at the First-tier Tribunal in late 2023 after the Court of Appeal had remitted the case for fresh consideration.

The case clarified two big points. First, the test of being “in business on own account” matters and can save a contractor even where MOO and control look unfavourable. Second, the court rejected HMRC’s attempt to import the Autoclenz approach (which lets courts ignore sham clauses in employment cases) into tax cases. Tax tribunals look at the written contract terms, then check whether they reflect reality. If the contract is genuine, it provides the starting point for deciding whether IR35 payments are due.

Basic Broadcasting Ltd v HMRC (Adrian Chiles): The Cost of Being Caught by IR35

Adrian Chiles won at the First-tier Tribunal in 2022. HMRC appealed. The Upper Tribunal in June 2024 sent the case back to be heard again. As of early 2026, after more than a decade of investigation, his case still isn’t fully resolved.

The point isn’t who wins. It’s the cost of being on the wrong end of an IR35 fight. Even when contractors win, they pay legal fees, lose years of their life, and live with the stress of potential IR35 payments liability hanging over them.

Professional Game Match Officials Ltd v HMRC (Supreme Court, September 2024): Latest IR35 Ruling

This case involved part-time football referees. The Supreme Court ruled that a simple work-for-pay exchange is enough for mutuality of obligation within an engagement. It also reaffirmed that contractual rights of control can matter even if they aren’t always used in practice.

PGMOL settled years of debate about the latest IR35 case law. After it, HMRC has a clearer roadmap for determining whether a contractor is employed for tax purposes, and so do businesses.

Table 3: Recent IR35 Cases at a Glance

| Case | Year decided | Outcome | Key takeaway |

|---|---|---|---|

| HS2 Ltd | 2024 | £6.2m settlement | CEST alone is not a defence |

| DWP, MOJ, Home Office | 2018 to 2023 | £180m+ combined | Public sector bodies often hit first |

| Atholl House (Kaye Adams) | 2023 | Contractor won | “In business on own account” can save the day |

| Basic Broadcasting (Chiles) | Ongoing since 2017 | Remitted again in 2024 | Even winners pay heavily in time and stress |

| PGMOL | 2024 (Supreme Court) | HMRC view confirmed | Work-for-pay is enough for MOO |

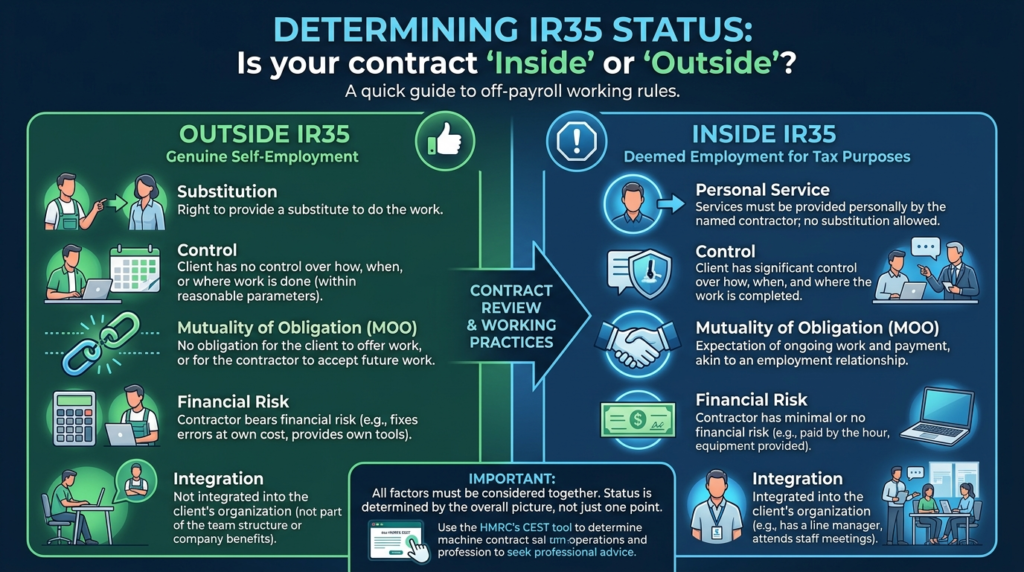

Chapter 4: The Gap Between Paper and Practice — Where a Contract Falls Inside or Outside IR35

Now the part most articles miss.

A well-drafted contractor agreement is necessary. It is not sufficient. HMRC and the tribunals look at the working reality, then test it against the contract. If the two don’t match, the contract loses — and IR35 payments become due.

Think of any contractor engagement as having three layers.

The Three-Layer Model for Status Determination

Layer 1: The Written Contract The signed agreement. Substitution clauses, control language, statements about no MOO, exclusion of employee benefits. This is where most legal effort goes.

Layer 2: The Working Reality What actually happens day to day. Who reports to whom? Where does the work happen? Is the contractor working on internal Slack channels, attending all-hands meetings, included in the team rota? Do they use company-issued laptops? Are they doing the same job as employees?

Layer 3: The Evidence Trail What you can prove if HMRC asks. Status Determination Statement, working notes, emails about scope changes, invoices, deliverable acceptance records, proof the contractor is operating as an independent business with other clients.

Most businesses focus on Layer 1, ignore Layer 2, and forget about Layer 3 entirely.

The Drift Problem: How Working Inside IR35 Happens Gradually

Most contractors don’t start out looking like employees. They drift there. Three patterns cause it.

Scope creep. A six-month project to build a new system runs over. Then there’s a list of “small” follow-on tasks. Two years later, the contractor is still there, doing whatever the team needs that week — effectively working inside IR35 without anyone noticing.

Integration. The contractor joins the daily standup. They get a company email address. They are added to the org chart. They sit in performance reviews of their own deliverables, sometimes of permanent staff. None of this happens by design. It happens because it is convenient.

Loss of substitution. A contractor who could once send a substitute now has key knowledge no one else has. Even if your contract still permits substitution, in reality, no replacement could pick up the work.

Each step is small. The cumulative effect is that an “outside IR35” engagement, set up cleanly, becomes a textbook inside IR35 case over 18 months — with backdated IR35 payments the consequence.

How to Spot the Drift: Whether a Contractor Is Really an Employee of the End Client

A simple test. Pick a contractor who has been with you for over a year. Ask the line manager:

- If the contractor were sick for two weeks, what would happen?

- Could a substitute step in?

- How is their work checked or signed off?

- What hours do they keep?

- Where do they work?

If the answers are indistinguishable from those about a permanent employee, the engagement has drifted. The contractor and the client relationship now looks like employment, and the correct amount of tax should be collected through IR35 payments on the payroll.

Table 4: The Drift in Practice

| Started as | Drifted to | IR35 effect |

|---|---|---|

| Project-based, deliverables agreed | Open-ended, “do what’s needed” | MOO and control increase |

| Worked from own office, own laptop | Issued a company laptop, sits at a desk in the office | Control increases |

| Substitution clause active and tested | Substitution never used, role is contractor-specific | Personal service strengthens |

| Contractor had multiple clients | This client takes 80%+ of contractor’s revenue | “In business on own account” weakens |

| Reported to project sponsor | Now in same line management as employees | Control increases |

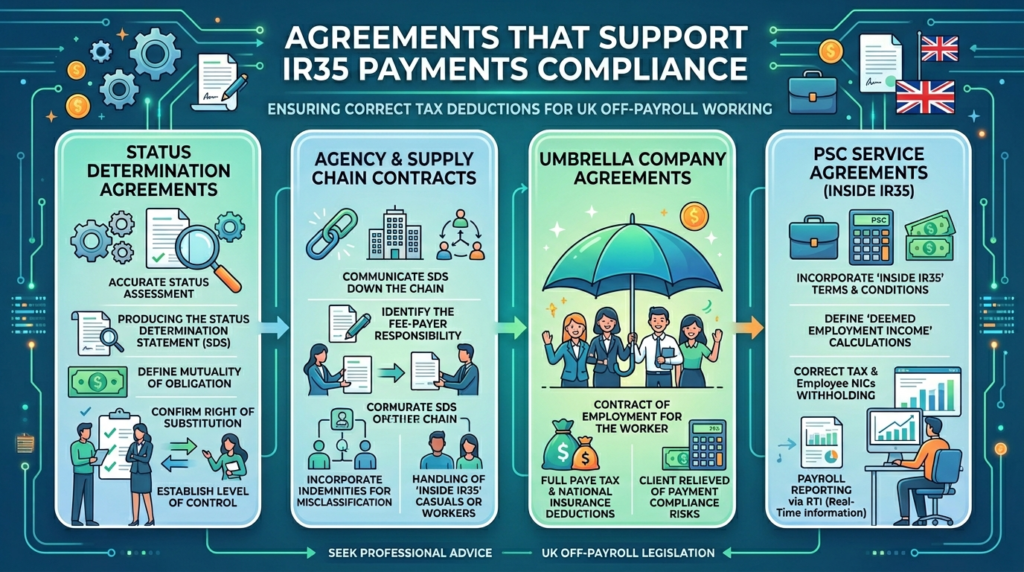

Chapter 5: Drafting Contractor Agreements That Support IR35 Payments Compliance

The contract still matters. It is your starting point and, if challenged, your first line of defence. Five drafting principles will get you most of the way.

Principle 1: Use a Statement of Work, Not an Open Framework

Many businesses use a master services agreement (MSA) with rolling Statements of Work (SoWs). This works in IR35’s favour if each SoW describes a defined deliverable, a fixed price or capped fees, and a clear end point. It works against you if the SoW says “consultancy services as required” with hourly billing.

A good SoW is project-shaped. A bad SoW reads like a job description — and if a contract is deemed to be employment for tax purposes, IR35 payments must be processed through PAYE.

Principle 2: Make Substitution Real, Not Theoretical

Many contracts include a substitution clause that the parties never test. A clause that requires the client’s approval, with no criteria for refusal, is weak. Better drafting:

“The Contractor may provide a suitably qualified substitute to perform the Services. The Contractor shall remain responsible for the substitute’s work and shall continue to bear the cost of providing the Services. The Client shall not unreasonably refuse a substitute who meets the qualifications set out in Schedule 1.”

Even better: actually use it once, on a small piece of work. A used substitution clause is far stronger than an unused one — and strongly supports a finding that the engagement falls outside IR35.

Principle 3: Be Explicit About Control

The contract should make clear that the contractor controls how the services are provided. The client controls what the deliverable is, when it is needed, and the standard it must meet. The line is between “what” and “how”.

Avoid wording that puts the contractor inside the client’s management chain. References to “the Contractor will report to [Manager]”, “follow our working hours”, or “attend our team meetings” cause problems when determining whether IR35 applies.

Principle 4: Don’t Dress Up Benefits

Contractors should not get holiday pay, sick pay, pension contributions, training budgets, or perks like gym memberships and birthday vouchers. If your finance system pays a contractor on a public holiday at the normal rate, you have a problem. Contractors invoice for work done — they are not classed as an employee for tax and NIC purposes. IR35 payments reflect this distinction: either you pay the contractor’s company for services, or you must pay tax and employee national insurance as an employee through PAYE.

Principle 5: Build in a Real End

Indefinite engagements are a red flag. A clause that allows automatic renewal “unless terminated” is weaker than one that requires a fresh SoW to be signed for any new work. The latter forces a fresh look at the engagement each cycle, including a reassessment of whether IR35 applies and how IR35 payments should be handled.

Drop-In Clauses

Three sample clauses you can adapt:

Substitution clause: “The Contractor may, at its discretion, provide a substitute to perform any part of the Services. The Contractor shall: (a) inform the Client in writing of the proposed substitute; (b) remain responsible for all Services performed by the substitute; (c) bear all costs associated with the substitute’s engagement. The Client may refuse a proposed substitute only on reasonable grounds relating to suitability, qualifications or security clearance, with such grounds to be stated in writing.”

Control and method clause: “The Contractor shall determine the manner, method, sequence and means of performing the Services. The Client shall be entitled to specify the deliverables, deadlines and standards of acceptance, but shall not direct the Contractor as to how the Services are performed.”

No employee status clause: “The Contractor is engaged as an independent contractor. Nothing in this Agreement shall create a relationship of employer and employee, principal and agent, or partnership between the parties. The Contractor shall not be entitled to participate in any employee benefits scheme operated by the Client, including any pension, sick pay, holiday pay, bonus or training entitlements.”

These clauses help only if the working practice matches them. Where services are provided in a manner inconsistent with the contract, the tax treatment changes and IR35 payments obligations follow.

Table 5: Strong Versus Weak Clause Drafting

| Issue | Weak version | Stronger version |

|---|---|---|

| Substitution | Subject to written approval at the Client’s sole discretion | Client may refuse only on reasonable grounds relating to suitability, with reasons given |

| Control | The Contractor will follow the Client’s reasonable instructions | The Contractor controls the manner and method of performance; Client sets deliverables and standards |

| Term | Continues until terminated by either party | Tied to a specific Statement of Work with defined deliverables and end date |

| Personal service | The Contractor agrees to provide the Services personally | The Contractor may provide the Services through any suitably qualified person |

| Benefits | Silent on benefits | Express exclusion of all employee benefits |

Chapter 6: Building a Compliance System for IR35 Payments That Holds Up

Drafting good contracts is one part. Running a compliance system is the other. Here is what an audit-ready process looks like.

Step 1: Centralise the Status Determination Decision

In many businesses, line managers hire company contractors. Each manager makes their own call on IR35 status. This is how blanket inside IR35 decisions happen, or worse, how contractors get classified outside IR35 without any process at all.

Better: a central HR or legal function responsible for determining the employment status of each engagement, based on input from the hiring manager. The same person or team should decide every case. Consistency is part of your defence.

Step 2: Use CEST, but Don’t Rely on It to Determine the IR35 Status

The HMRC tool was updated in spring 2025 and is more useful than before, but it doesn’t capture the full picture. Some businesses supplement CEST with an IR35 calculator tool for additional assurance. A standard process should:

- Run CEST and save the output

- Run a second independent assessment, using either a paid tool or a written review

- Compare both and resolve any conflicts

- Document the reasoning, even when it agrees with CEST

If CEST gives you “outside IR35” but your independent review says “inside”, you don’t get to pick the friendlier answer. You investigate and decide — because incorrect IR35 payments processing carries real consequences.

Step 3: Issue the SDS Properly

The Status Determination Statement must:

- State the conclusion (inside or outside IR35)

- Give reasons that show you actually thought about the IR35 status of a contract

- Be sent to the contractor

- Be sent to any agency in the supply chain

A boilerplate SDS that says “this engagement is outside IR35 based on standard factors” is not enough. You must demonstrate you are responsible for determining IR35 status and have done so properly.

Step 4: Run a Real Disputes Process

Contractors have a legal right to challenge an SDS, and the contractor has an obligation to raise any dispute within the specified timeframe. You must have a process. The decision-maker on disputes should be different from the original assessor where possible. Decisions must be in writing, with reasons, within 45 days. Failure to respond means IR35 payments liability can transfer up the chain.

Step 5: Review at Each Renewal

IR35 status can change. A six-month outside IR35 engagement might still be outside IR35 at month 18, but the analysis must be redone. Tie this to the renewal of each SoW. Don’t auto-roll status decisions — particularly where the take-home pay structure or working arrangements have shifted.

Step 6: Spot-Check Working Practices

This is where most companies fall short. Once a quarter, audit a sample of contractor relationships. Talk to the line managers. Ask the questions in Chapter 4. If a contractor has drifted, fix it before HMRC arrives — either by restructuring the engagement so it genuinely falls outside IR35, or by bringing IR35 payments into compliance through payroll.

Table 6: A 12-Month Compliance Cycle

| Month | Action |

|---|---|

| 1 | Annual policy review; train managers on IR35 basics |

| 3 | Spot-check sample of active contractor engagements |

| 6 | Review CEST outputs against case law updates |

| 9 | Audit SDS quality on past 6 months of engagements |

| 12 | End-of-year compliance report; risk register update |

| Ongoing | New engagement: full status process; renewals: refreshed SDS |

Chapter 7: When HMRC Comes Knocking Over IR35 Payments

If you are doing things right, an HMRC investigation should be uncomfortable but survivable. Here is how to handle one.

The First Letter

HMRC usually opens with a letter asking about your IR35 processes and how you handle IR35 payments. It is not a tax demand. It is a request for information. The letter typically asks:

- How you assess IR35 status

- What tools you use

- Your written policies

- A sample of SDS documents

- Information about specific contractors

You usually have 30 to 45 days to respond. Don’t ignore it. Don’t reply without legal or tax advice.

What HMRC Will Look For

Investigators are trained to spot:

- Blanket determinations (everyone inside or outside without case-by-case analysis)

- Sole reliance on CEST

- Contracts that don’t match working reality

- Missing or boilerplate SDS documents

- No evidence of a disputes process

- Contractors who have been in place for years on similar terms

- Incorrect IR35 payments — whether too little tax and national insurance has been deducted

The Offset Rule in Practice for IR35 Payments

If HMRC concludes your assessment was wrong, the financial impact will follow the April 2024 offset rule. The IR35 payments bill will be:

- The PAYE that should have been paid (the correct amount of tax and national insurance contributions)

- Less the tax already paid by the contractor’s PSC

- Plus interest

- Plus any penalty

Penalties depend on whether HMRC sees the error as careless, deliberate or concealed. Careless errors typically attract 0% to 30% penalties. Deliberate errors run 20% to 70%. Concealment can hit 100%.

The post-April 2024 picture is much friendlier than before, but interest still bites and penalties still hurt.

Settlement Versus Tribunal

Most IR35 disputes settle. Tribunal is expensive, slow and public. If HMRC’s case is weak or based on a misreading of your documents, push back. If your evidence is genuinely thin, settle on the best terms you can negotiate.

The case of Adrian Chiles shows the cost of fighting all the way. Win or lose, you pay heavily in time and money.

Document Preservation

The moment you receive an HMRC enquiry letter about IR35 payments:

- Stop deleting any contractor-related communications

- Preserve all SDS documents, CEST outputs, and review notes

- Keep all signed contracts and SoWs

- Hold onto invoices, time records, and project documentation

- Retain emails about scope, deliverables, and substitution

HMRC can look back four to six years for careless errors, and up to 20 years for deliberate ones. At the end of the tax year, ensure all IR35 payments records are properly archived.

Table 7: A Typical HMRC Investigation Timeline

| Stage | Timeframe | What to do |

|---|---|---|

| Opening letter | Day 1 | Acknowledge, do not panic, instruct advisers |

| Information request | Days 30 to 45 | Respond fully, with reasons |

| Document review | 2 to 6 months | Provide further evidence as requested |

| HMRC view of position | 6 to 12 months | Decide whether to challenge or settle |

| Settlement or appeal | 12 to 24 months | Apply offset rule; negotiate penalty rate |

| Tribunal (if pursued) | 2 to 5 years | Substantial cost, public ruling |

Closing Thoughts

IR35 has been treated as a technical tax problem for 25 years. That is the wrong frame. It is a relationship problem. The question isn’t really how a contract is worded. It is how a working relationship operates — and whether IR35 payments are being handled correctly.

The April 2024 offset rule and the September 2024 PGMOL Supreme Court decision have settled some of the noise. The new IR35 landscape means the rules are clearer than they have been since 2000. The risk is more manageable than at any point since 2017. But the temptation to slip back into bad habits — blanket bans, careless determinations, contracts that bear no resemblance to reality — is still there.

The businesses that get IR35 payments right in the next few years will be the ones that treat compliance as ongoing operational hygiene, not an annual paperwork exercise. They will write better contracts, yes. But they will also watch how those contracts are lived out. Whether a contractor provides services through an umbrella company, or chooses to work through a limited company, the underlying off-payroll working rules and IR35 payments obligations remain the same.

Frequently Asked Questions

1. Has the Latest IR35 Legislation Been Scrapped?

No. There were rumours in 2024 and 2025, but the IR35 rules remain in force. From April 2025, the small company financial threshold rose, meaning more businesses will eventually fall outside the off-payroll working rules. Because IR35 looks back at your previous financial year, the earliest most affected medium-sized businesses will see this take effect is the 2027/28 tax year. If contractors work through an umbrella company, different IR35 payments arrangements apply — the umbrella company handles payroll and must pay tax and national insurance contributions before passing on take-home pay to the worker.

2. We are a small company. Do the off-payroll working rules apply to us?

If you meet the small company test (currently based on turnover, balance sheet total and employee headcount under the Companies Act 2006), you are exempt from Chapter 10 of ITEPA 2003. But the original IR35 rules from 2000 still apply to your contractors, who must self-assess their own status under Chapter 8. Contractors are responsible for calculating their own deemed salary and processing their own IR35 payments in this scenario. You should still keep clear records of your own size, because contractors and agencies are entitled to ask you to confirm it.

3. Can we just rely on the HMRC CEST tool to determine the IR35 status?

No. CEST is a starting point. The HS2 case (£6.2 million settlement) shows that sole reliance on CEST is risky. Pair it with an independent review and document your reasoning. HMRC will only stand by a CEST outcome if the answers given to it match working reality, and that is a matter of fact, not a matter of trust. Whether a contractor is working inside or outside IR35 determines how IR35 payments must be handled — and who is responsible for deciding whether IR35 applies.

4. What changed with the April 2024 offset rule for IR35 payments?

If HMRC overturns an outside IR35 decision, the IR35 payments bill is now reduced by the tax the contractor’s PSC has already paid. The practical risk has fallen by roughly 75%. Penalties and interest still apply, and a careless or deliberate error can still bring a sizeable bill, but the disproportionate liability that drove blanket bans after the 2021 IR35 changes is largely gone. Any tax advantage previously gained by incorrect classification is effectively clawed back, but without the punitive doubling that existed before.

5. Our contractor has worked with us for three years. Are they automatically inside IR35?

Length of engagement is a factor, not a decider. Long engagements raise the risk of “drift” into employment-like working inside IR35. Run a fresh status review, look hard at the working practices, and check if substitution and project-based working still apply. If they do, an outside IR35 engagement can survive a long term — and IR35 payments through PAYE are not required. If they don’t, the right answer is to fix the arrangement (or move the role to PAYE with proper IR35 payments processing), not to hope HMRC won’t notice. The contractor has an obligation to cooperate with any status review, and both the contractor and the client share an interest in getting it right.